Government Budgets Face Major Disruptions from Tax Assessment Appeals

The Pennsylvania Lawyer, July/August 2024

‘Some Kind of Systemic Breakdown:’ Property Owners Waiting Months for Assessment Refunds that Should Arrive in Just 30 Days

Pittsburgh Post-Gazette, May 16, 2024

No letup: City, school district could be dealing with more building assessment cuts in 2024

Pittsburgh Post-Gazette, April 18, 2024

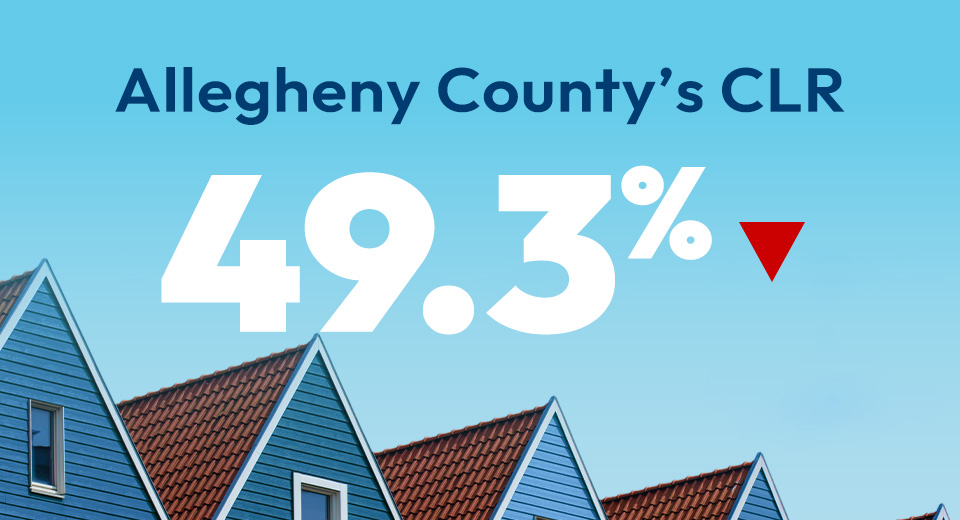

Unpacking Allegheny County Tax Assessment Appeals: Helping Clients Secure Savings in 2024

The Legal Intelligencer, March 29, 2024

‘A big number’: Allegheny County Council action could trigger thousands of assessment appeals — retroactively

Pittsburgh Post Gazette, January 26, 2023

2023 Tax Assessment Appeal Deadlines Fast Approaching In Many Western Pennsylvania Counties

MUS Client Advisory, July 19, 2022

In 2023, tax breaks could await property owners who file assessment appeals in Allegheny County

Pittsburgh Post-Gazette, June 30, 2022

Owners of Downtown Pittsburgh skyscrapers, other commercial properties could benefit from assessment appeals deal

Pittsburgh Post-Gazette, May 9, 2022

Empty Office Buildings Squeeze City Budgets as Property Values Fall

The New York Times, March 3, 2021

COVID-19 Fallout Could Lead to Lower Commercial Property Taxes

Bloomberg Tax, July 14, 2020

Jason M. Yarbrough

Partner

Jason M. Yarbrough is a Partner and Chair of the firm’s Real Estate Litigation Section, Co-Chair of the firm’s Summer Associate Program, and a member of the firm’s Construction Law, Creditors’ Rights & Bankruptcy, Energy, Utilities & Mineral Rights and Litigation and Dispute Resolution Practice Groups.

Jason frequently represents clients in complex commercial, real estate and construction disputes. His real estate litigation practice includes disputes involving the acquisition and development of real property, landlord tenant disputes, property rights, property tax assessment appeals and exemption proceedings, land use and title disputes, partition actions and foreclosure proceedings. In his construction practice, Jason represents owners, developers, contractors, architects, and engineers in disputes arising out of both public and private construction projects. He has litigated claims in state and federal courts, and against state agencies and the federal government.